The Fed’s Waller and Logan lay out some basic principles.

By Wolf Richter for WOLF STREET.

On Friday, Christopher Waller, member of the Federal Reserve Board of Governors, and Dallas Fed president Lorie Logan laid out some broad principles how far and how fast QT could or should go in order to “normalize” the balance sheet, how they would try to avoid an “accident” along the way so that QT could go on for longer, and how they might deal with a future emergency by doing QE without increasing the balance sheet.

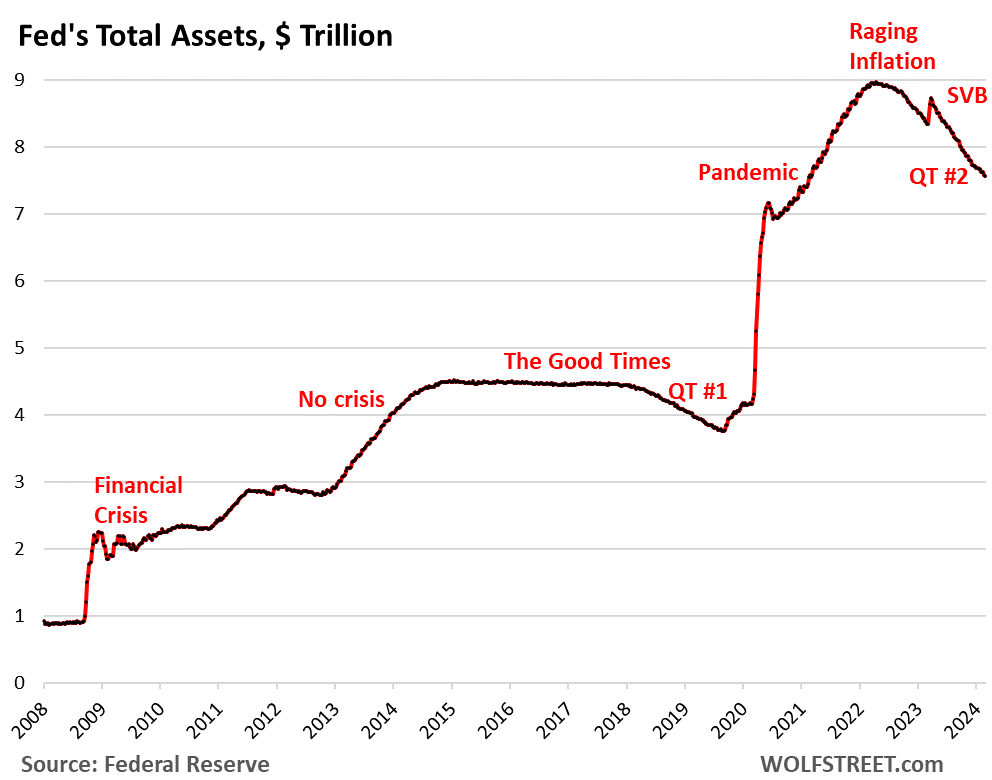

So far, QT has removed $1.40 trillion from the Fed’s balance sheet since the peak in April 2022. Total assets are now down to $7.57 trillion:

The principles they laid out.

In the FOMC minutes, released on February 22, the Fed had already outlined some basic ideas: The Fed Wants to Drive QT as Far as Possible Without Blowing Stuff Up, and it’s Working on a Plan. In their speeches, Waller and Logan provided a lot of additional material and principles. So here we go.

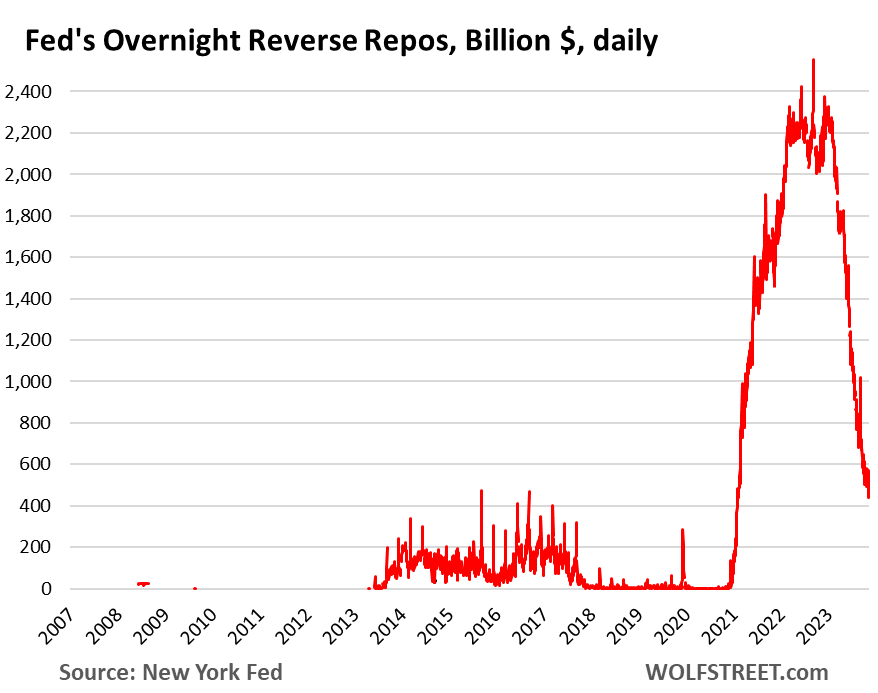

ON RRPs should go back to zero. These overnight reverse repurchase agreements signify “excess liquidity that financial market participants do not want,” Waller said in his speech. Logan confirmed in her speech; she expects them to be “drained.”

So the facility should go back to where it was, namely at or near zero. This means that close to $500 billion in QT would be required to wring out that “unwanted” excess liquidity.

MBS should “go to zero,” Waller said. This means that even after the Fed ends QT sometime in the future, MBS should continue to run off via the pass-through principal payments as underlying mortgages are paid off (sale of the home or refi), or are paid down (mortgage payments). “I believe it is important to see a continued reduction in these holdings,” Waller said. After QT ends, the MBS that run off would then be replaced with Treasury securities.

The Fed already did this before. After it ended QT-1 in the summer of 2019, MBS continued to run off the balance sheet and were replaced by Treasury securities until the pandemic QE began in March 2020 (our comment and chart of this period).

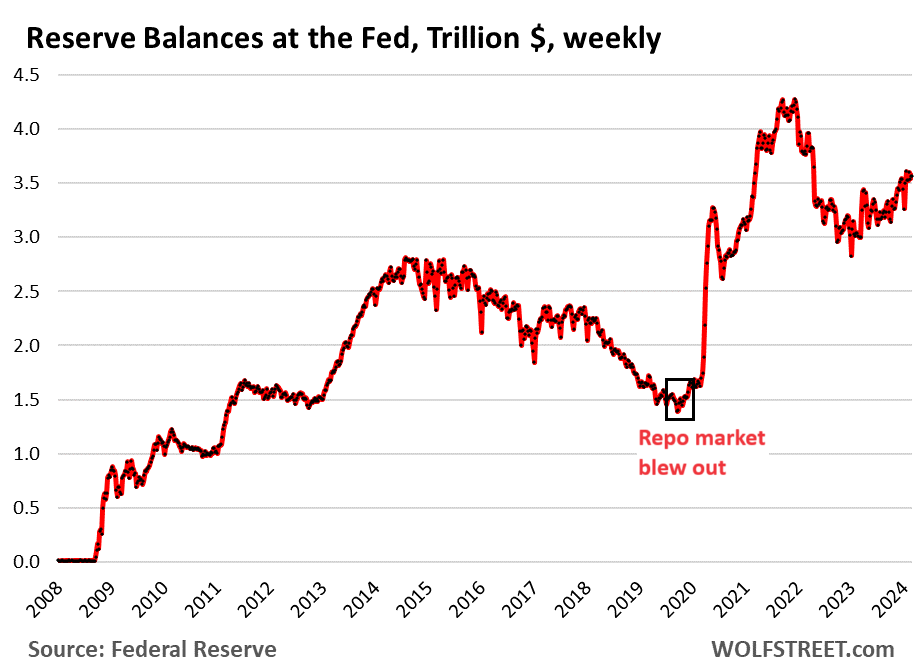

Reserves should drop after ON RRPs vanish. Reserves are cash that banks put on deposit at the Fed and represent bank liquidity. They could drop a lot because they’re essentially back to where they had been before QT started and have not absorbed any QT yet. QT was absorbed so far by ON RRPs.

During QT-1, reserves dropped a little below $1.5 trillion, which caused banks to stop lending to the repo market, which caused the repo market to blow out in September 2019 (black box in the chart below). So this was a sign that reserves were no longer “ample,” that they had been drawn down too far.

What does “ample” even mean: “The word ‘ample’ suggests comfortably but efficiently meeting banks’ demand,” Logan said. “The Fed’s operating regime is intended to supply ample reserves to banks—but only ample reserves and not more than that,” she said. But “the ample level of reserves is unknown,” she said.

The new Standing Repo Facility “may allow banks to lower the level of reserves below what reserves would be without the facility,” Waller said. The SRF prevents the repo market from blowing out even if reserves drop too far.

The Fed had an SRF through 2008. It was used to deal with market issues, including during 9/11 when markets were shut down. Repos mature within a relatively short term, such as within a day or within a week, and if they’re not rolled over, they vanish from the balance sheet and don’t get stuck on the balance sheet for years or decades like QE assets.

But in 2009, the Fed shut down its SRF because it wasn’t needed amid QE at the time. Then the Fed didn’t revive the SRF when QT-1 started in 2017, and in September 2019, the repo market blew out. So the Fed revived its SRF in July 2021 in preparation for QT-2.

The SRF “may provide a signal for when…

This article was originally published by a wolfstreet.com . Read the Original article here. .