PM Images

Long-time readers know I’ve been bullish on senior loans and other variable rate investments for years. These have performed exceedingly well too, as Federal Reserve hikes have led to significant dividend growth with almost no impact on prices. As the Fed is poised to cut rates in the coming months, thought to have another look at senior loans, to see if these remain viable investments under more unfavorable macro conditions.

Right now, senior loans yield 2.0% – 3.0% more than fixed-rate bonds of comparable credit risk. For senior loans to yield less than these securities, the Fed would have to cut by 2.0% – 3.0%. Current Fed guidance has this occurring in 2026, at the earliest.

Senior loan offer investors competitive yields, even after discounting likely Fed cuts. As such, these remain strong investment opportunities, and buys. More dovish investors might disagree.

I’ll be focusing on the Invesco Senior Loan ETF (NYSEARCA:BKLN), the largest senior loan ETF in the market, for the remainder of the article, but everything here should apply to most senior loan funds in roughly equal measure.

BKLN – Quick Overview and Investment Thesis

BKLN is the largest senior loan ETF in the market.

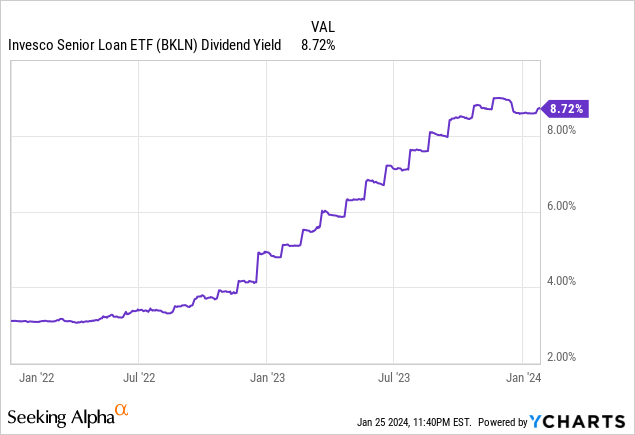

Senior loans are almost always senior secured variable rate loans from non-investment grade corporations. Simplifying things a bit, variable rate loans are indexed to specific benchmark rates, and see higher coupon rates when the Federal Reserve hikes rates. BKLN’s yield has increased by 5.6% since the Fed started to hike, in-line with Fed hikes.

Most bonds have fixed rates from issuance until maturity. In most cases, for bond investors to take advantage of rising rates they need to wait until their bonds mature, to replace them with newer, higher-yielding alternatives. It is a much slower process, which results in slower dividend growth for most bond funds compared to BKLN.

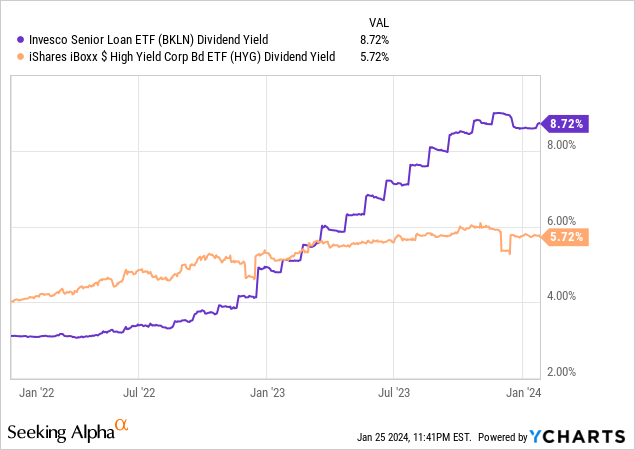

As an example, the iShares iBoxx $ High Yield Corporate Bond ETF (HYG), the largest high-yield bond ETF, has seen its yield increase by 1.7% since the Fed started to hike, around 1/3rd of the growth experienced by BKLN.

Senior loans are almost always from non-investment grade corporations. These account for 98% – 99% of BKLN’s portfolio, with an average credit rating of B. Credit quality is broadly low, which increases risk, volatility, and losses during downturns and recessions.

BKLN

High credit risk means high yields, with senior loans as an asset class yielding 10.6%. This is highest amongst most bond sub-asset classes, and by quite a wide margin.

JPMorgan Guide to the Markets

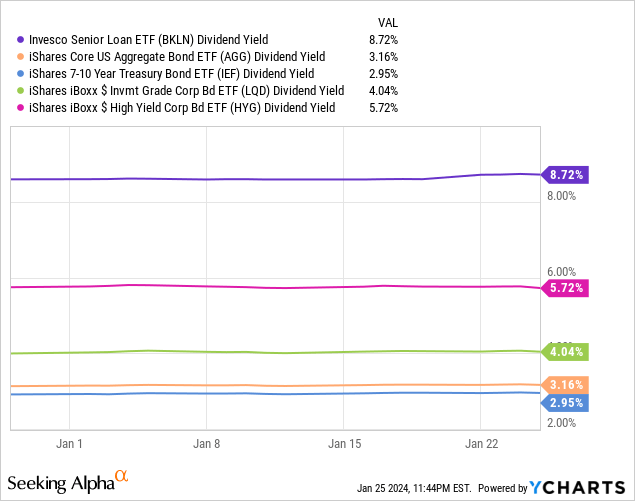

BKLN itself also yields more than most of the larger bond index funds, including those focused on high-yield bonds.

BKLN’s investment thesis is quite simple. The fund offers investors a strong, growing 8.7% yield, higher than most relevant bonds and bond sub-asset classes.

BKLN’s most significant risk or issue is also simple. The fund’s dividends should decline once the Fed cuts rates, which will very likely happen in the next few months. BKLN seems to yield more than enough to withstand these cuts, however. Let’s have a closer look at these issues.

Senior Loans Versus High-Yield Bonds

Asset Class Yield Comparison

Senior loans and high-yield corporate bonds should have broadly similar yields, as both have similar credit risk. This is indeed generally the case, with these securities trading with an average spread of 0.20% these past ten years.

JPMorgan Guide to the Markets

Considering the above, I think it would be fair to say that senior loans are attractively priced when these yield more than high-yield bonds, and vice versa.

Senior loans currently yield 3.0% more than high-yield bonds, and would continue to yield more if the Fed were to cut rates by less than 3.0%. Current Fed guidance is for long-term rates to stabilize around 2.75% – 3.0% lower than today. Under current Fed guidance, senior loans would continue to yield more…

This article was originally published by a seekingalpha.com . Read the Original article here. .